Annuities provide a series of income payments in exchange for premiums paid upfront. Many annuities also undergo an accumulation phase in which the value of the premiums grows tax-deferred. Annuities can help protect against the risk of outliving your savings.

Jennifer Schell, CAS® Financial Writer, Certified Annuity Specialist® Jennifer Schell is a professional writer focused on demystifying annuities and other financial topics including banking, financial advising and insurance. She is proud to be a member of the National Association for Fixed Annuities (NAFA) as well as the National Association of Insurance and Financial Advisors (NAIFA). Read More

Lamia Chowdhury Financial Editor Lamia Chowdhury is a financial editor at Annuity.org. Lamia carries an extensive skillset in the content marketing field, and her work as a copywriter spans industries as diverse as finance, health care, travel and restaurants. Read More

John Stevenson, CFF Owner and Advisor at Stevenson Retirement Solutions John Stevenson, a Certified Financial Fiduciary®️, specializes in securing retirements with tax-free accounts. With a focus on guaranteed retirement, he's ensured none of his clients suffer from market fluctuations. As a renowned educator and podcast host, John empowers thousands weekly, sharing his expertise in minimizing taxes and protecting against financial downturns. Read More

Fact Checked Fact CheckedAnnuity.org partners with outside experts to ensure we are providing accurate financial content.

These reviewers are industry leaders and professional writers who regularly contribute to reputable publications such as the Wall Street Journal and The New York Times.

Our expert reviewers review our articles and recommend changes to ensure we are upholding our high standards for accuracy and professionalism.

Our expert reviewers hold advanced degrees and certifications and have years of experience with personal finances, retirement planning and investments.

How to Cite Annuity.org's ArticleAPA Annuity.org (2024, August 14). How Do Annuities Work? Retrieved September 16, 2024, from https://www.annuity.org/annuities/how-they-work/

MLA "How Do Annuities Work?" Annuity.org, 14 Aug 2024, https://www.annuity.org/annuities/how-they-work/.

Chicago Annuity.org. "How Do Annuities Work?" Last modified August 14, 2024. https://www.annuity.org/annuities/how-they-work/.

Why Trust Annuity.org Why You Can Trust Annuity.orgAnnuity.org has provided reliable, accurate financial information to consumers since 2013. We adhere to ethical journalism practices, including presenting honest, unbiased information that follows Associated Press style guidelines and reporting facts from reliable, attributed sources. Our objective is to deliver the most comprehensive explanation of annuities and financial literacy topics using plain, straightforward language.

We pride ourselves on partnering with professionals like those from Senior Market Sales (SMS) — a market leader with over 30 years of experience in the insurance industry — who offer personalized retirement solutions for consumers across the country. Our relationships with partners including SMS and Insuractive, the company’s consumer-facing branch, allow us to facilitate the sale of annuities and other retirement-oriented financial products to consumers who are looking to purchase safe and reliable solutions to fill gaps in their retirement income. We are compensated when we produce legitimate inquiries, and that compensation helps make Annuity.org an even stronger resource for our audience. We may also, at times, sell lead data to partners in our network in order to best connect consumers to the information they request. Readers are in no way obligated to use our partners’ services to access the free resources on Annuity.org.

Annuity.org carefully selects partners who share a common goal of educating consumers and helping them select the most appropriate product for their unique financial and lifestyle goals. Our network of advisors will never recommend products that are not right for the consumer, nor will Annuity.org. Additionally, Annuity.org operates independently of its partners and has complete editorial control over the information we publish.

Our vision is to provide users with the highest quality information possible about their financial options and empower them to make informed decisions based on their unique needs.

Annuities are insurance products that provide a reliable, steady stream of payments to support your financial needs for the rest of your life or for a predetermined number of years. Because they are contracts, you can also customize them to meet your specific needs and fit your risk tolerance.

Annuities are not for everyone. However, if you’re nearing retirement and need to ensure you can pay your living expenses after you’ve stopped working, an annuity may fulfill those needs.

Annuities can be categorized into different types based on their features. One way to think about annuities is in terms of when the contract is annuitized, or converted into an income stream.

Immediate annuities, as the name suggests, annuitize right after the contract is issued, so owners can receive payments right away.

Steps for How an Immediate Annuity Works

These are the simplest type of annuities, compared to deferred annuities.

Is An Annuity Right For You?

Our short quiz provides clarity on whether an annuity is a smart choice for your retirement portfolio.

Deferred annuities accumulate value on the premium or premiums paid before converting the contract’s value into income payments. These products work differently depending on how the annuity’s value accumulates.

The interest that deferred annuities earn has the advantage of tax deferral. This means you won’t owe any taxes on an annuity’s growth until you receive income from the annuity. In the long run, tax deferral can lead to greater growth because more money is left in the account to compound value.

The tax deferment feature of annuities makes them ideal for high-net-worth individuals, like Ron in this example.

Name: Ron

Age: 55

Income: $180,000/year

Best Option: Deferred Annuity

Ron’s annuity can earn interest while he’s still working, and he won’t have to pay taxes on that income while he’s still in a higher tax bracket. When the contract annuitizes after Ron retires, he’ll likely be receiving less income and, therefore, could be in a lower tax bracket.

As a result, he’ll end up paying less tax on his annuity earnings than he would on something like a certificate of deposit (CD), which is taxed each year as interest accumulates.

The two most popular types of deferred annuities are fixed annuities and variable annuities.

John Stevenson, CFF Owner and Advisor at Stevenson Retirement SolutionsWhen a person is contemplating purchasing an annuity, they need to ask themselves what they are trying to accomplish. If the answer is that they want a fixed rate of returns, guaranteed lifetime income or the peace of mind of having some of their money in a “safe money” account, then an annuity could be the right choice.

John Stevenson, a Certified Financial Fiduciary®️, specializes in securing retirements with tax-free accounts. With a focus on guaranteed retirement, he’s ensured none of his clients suffer from market fluctuations. As a renowned educator and podcast host, John empowers thousands weekly, sharing his expertise in minimizing taxes and protecting against financial downturns.

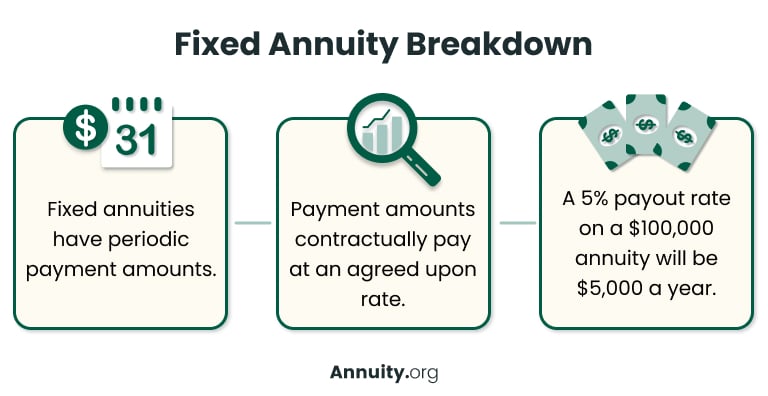

Fixed annuities work very similarly to CDs; you put money into the annuity and let it accumulate interest at a guaranteed rate for a set period. However, unlike a CD, a fixed annuity can be converted into a stream of income as opposed to a lump sum payout once it reaches maturity.

The rate a fixed annuity earns depends on the rates of the low-risk investments and bonds the insurer invests the annuity premiums in.

Steps of a Fixed Annuity

The most basic version of a fixed deferred annuity is based on a single owner’s life and the payments will end at their death. However, there are additional customizations available to create a contract that fits the owners’ needs.

For instance, it’s possible to include a spouse on the contract, which will make the payments last until both parties have passed away. Additionally, adding a “period certain” or “return of principal” rider to the contract will create a guaranteed return of money for the owners or their heirs regardless of how long they live.

Adding riders like these will lower the monthly payout, so compare your options before committing.

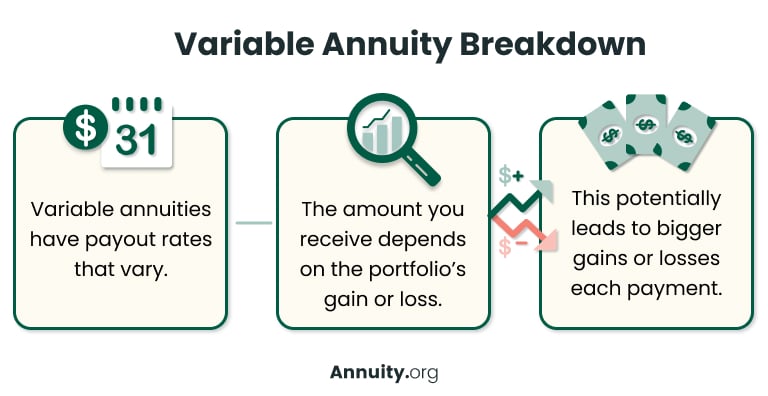

Variable annuities are specialized annuities that offer the owners more control over the underlying investments of their contracts. Variable deferred annuities, therefore, may offer higher rates of return when invested more aggressively, but they also require a higher risk tolerance because there are fewer or no guarantees.

Variable deferred annuities do not have a mandatory annuitization requirement and have no limits on the amount that can be contributed over time. One of the biggest benefits of this type of annuity is to supplement the retirement investments for individuals who are already maxing out their other retirement accounts.

Variable deferred annuities typically offer a pre-approved group of mutual funds or ETFs that the investor can invest in. Investment returns are market-based and the contract offers no guarantees on returns.

Because there are no guarantees of the annuity’s value, the income payments from a variable annuity will vary depending on the performance of an investment portfolio. The amount you receive in payments depends on how much money the portfolio gains or loses. This type of annuity is riskier but also has the potential to pay you more in a rising market environment.

It’s important to understand all the costs and rules associated with this type of product before buying it. In a falling market environment, your income payments will not stop, but they will be reduced. The costs associated with this type of product may degrade your ability to recover at the same rate as the market.

The type of annuity you purchase and the terms of your contract dictate exactly how you’ll be paid from your annuity. You typically receive the principal back from an annuity in the form of periodic annuity payouts.

Are annuities an investment or longevity insurance?An annuity is a financial product structured by a long-term contract between you and an insurance company. Annuities are part of a retirement strategy designed to provide you with a steady stream of guaranteed income in retirement.

Do annuities lose money when the stock market goes down?Market fluctuations have different effects on different types of annuities. Fixed annuities, for example, guarantee your returns no matter how the market performs. Other types, like variable annuities, carry more risk in down markets because their value is tied to the performance of underlying investments.

We may be compensated if you click this adOur free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

Please seek the advice of a qualified professional before making financial decisions. Last Modified: August 14, 2024 a phone call" width="360" height="240" />

a phone call" width="360" height="240" />

Learn More About Your Annuity Options

Our trusted annuity providers can help you earn up to 6.6%. Call Now: 877-918-7024 Written By Jennifer Schell, CAS® Financial Writer, Certified Annuity Specialist®Jennifer Schell is a professional writer focused on demystifying annuities and other financial topics including banking, financial advising and insurance. She is proud to be a member of the National Association for Fixed Annuities (NAFA) as well as the National Association of Insurance and Financial Advisors (NAIFA).